Subscribe to our research releases

Stay in touch with our latest insights, news and events.

The Time of Day Effect: A Breakthrough in Trading Cost Optimization

Introduction: The Time of Day Effect

Algorithmic traders have long focused on cost-saving opportunities like optimizing the speed of execution, intelligent order placement, liquidity curation, short-term alpha capture, and latency optimization. While these efforts have delivered incremental value, none match the potential of systematically exploiting the Time of Day Effect.

The Time of Day Effect refers to the variability in trading costs based on when a trade is executed during the trading day, holding participation rate constant. This is distinct from volume-driven effects, as many algorithms already spread orders proportionally in accordance with intraday volume. Our research reveals that even with constant order size and participation rate, trading costs vary significantly by time of day.

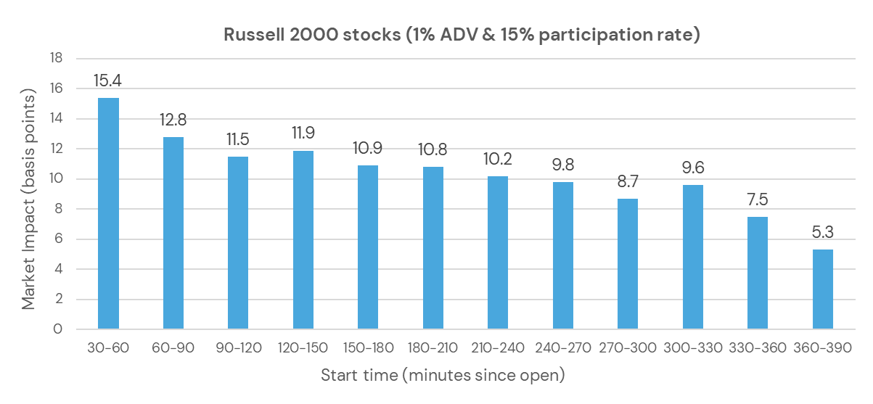

The Time of Day Effect is illustrated in Figure 1, where the data suggest distinct cost regimes: 9:30–10:00, 10:00–11:00, 11:00–2:00, and 2:00–4:00, with the last two hours showing the lowest average trading costs.

For this analysis, we utilize Trade and Quote (TAQ) data, from which we analyze the realized market impact of trading 1% of daily volume for Russell 2000 constituent stocks at a 15% participation rate starting at various times of day. Orders are constructed on these stocks using TAQ data to calculate trade imbalance, where for a given time period, the absolute difference between buy-driven volume (priced above midpoint) and sell-driven volume (priced below midpoint) constitutes an order of that size. An order’s size is its trade imbalance divided by the stock’s average daily volume; its participation rate is the trade imbalance over the interval volume during that period. The average execution price for the order is calculated from the trade data, and the order’s cost (market impact) is the difference between the interval VWAP and the midpoint price at the start of the order–arrival price.

The sample used to create Figure 1, for example, limits these orders to an average size of 1% of daily volume and fixes an average participation rate of 15%. We exclude the first 30 minutes of the day–well known for high costs (25 basis points of market impact for the same-sized orders shown in Figure 1)–to focus on the rest of the day.

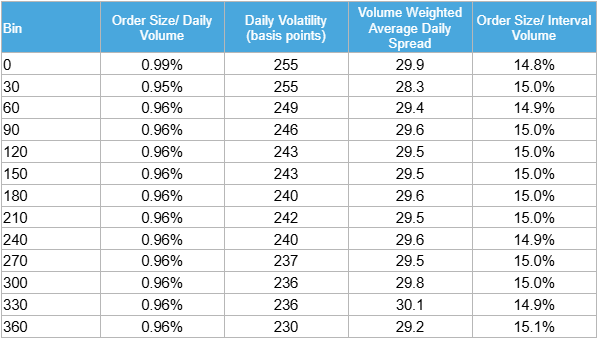

To ensure fair comparison, we have controlled for biases from stock selection, participation rates, order size, daily volume, average spread, and volatility, as illustrated in Table 1 in the Appendix. The TAQ dataset, with over 39 million meta-orders constructed from one quarter of trade data in 2024, allowed us to isolate 350,000 orders where only the time of day varied, confirming the existence of this effect.

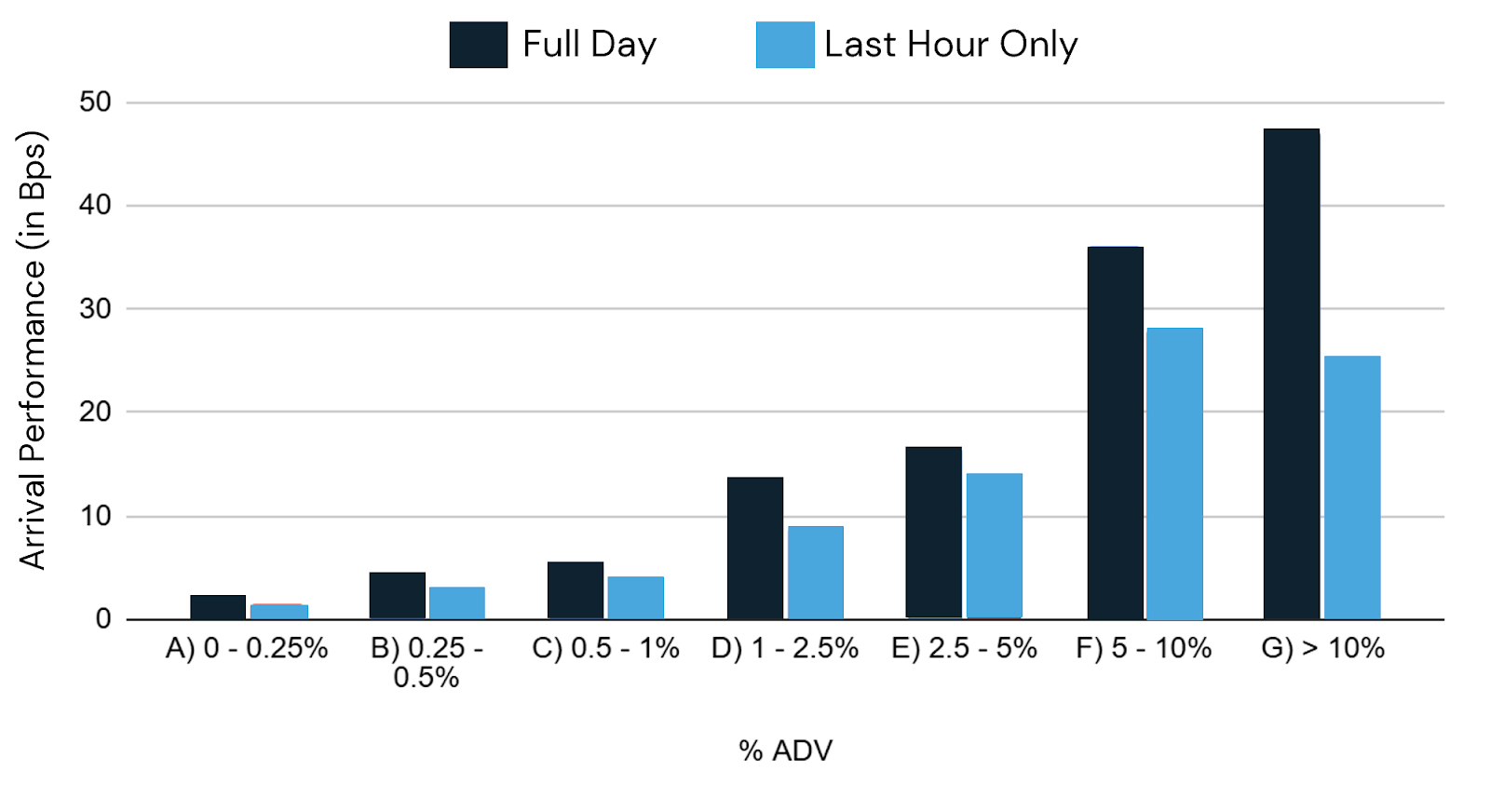

To validate the Time of Day Effect in our own execution data, we created a sample from four years of algo execution data. After filtering out limit orders and cancellations, the sample contained approximately 635,000 parent orders. We selected orders ending at market close and divided them into two subsets–those lasting at least six hours (lower participation rates) and those starting in the last hour (higher participation rates).

The results are striking. Orders starting in the last hour of the trading day incurred lower costs than those trading all day, despite their corresponding higher participation rates, as illustrated in Figure 2. While this corroborates the TAQ findings, execution data introduces its own biases. We have excluded canceled orders and tight limit orders to mitigate some of this bias, but other biases may persist. For example, we do not know whether we received a piece of an order or the entire parent order from a client. As a result, based on this data alone, one cannot make a leap of faith to avoid trading in earlier parts of the day–which makes the market data analysis so critical.

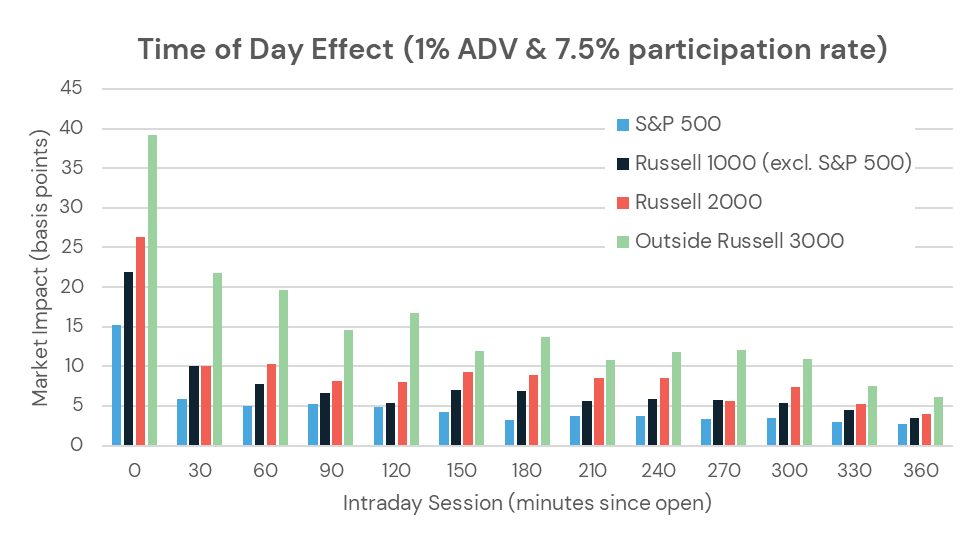

To test the effect’s persistence across liquidity levels, we analyzed stocks in the S&P 500, Russell 1000 (excluding S&P 500), Russell 2000, and stocks outside the Russell 3000, shown in Figure 3. While the magnitude of the Time of Day Effect is greater for less liquid stocks, the intraday cost pattern is consistent across liquidity levels. Notably illustrated in Figure 3, trading Russell 2000 stocks in the last two hours is less costly than trading S&P 500 stocks in the first hour.

Exploiting the Time of Day Effect to Reduce Trading Costs

The Time of Day Effect can be leveraged in two ways. A conservative approach would adjust trading proportions across the day without changing overall participation rates. A more aggressive approach would avoid high-cost time bins entirely, requiring careful analysis of the tradeoff between the increased participation rate and the avoidance of higher-cost bins.

Option 1: Changing the Schedule

We have already productized the first approach in our IS Zero algorithm. Unlike VWAP, which trades proportionally to volume, IS Zero uses an intraday schedule inversely proportional to market impact, capturing the Time of Day Effect beyond volume variations (as illustrated in Figures 1 and 2).

The results from IS Zero have been quite encouraging. From 2023 to Q1 2025, across more than 895,000 parent orders, on average, IS Zero reduced arrival slippage compared to the VWAP algorithm across all order size buckets, as shown in Figure 4. This sample includes all orders to IS Zero and VWAP algorithms between January 2023 and Q1 2025. We include only market orders trading for more than five minutes and executing more than $10,000. For a fairer comparison, we have normalized the arrival cost of each order by the associated interval spread in Figure 4.

Option 2: Aggressive Exploitation of the Time of Day Effect

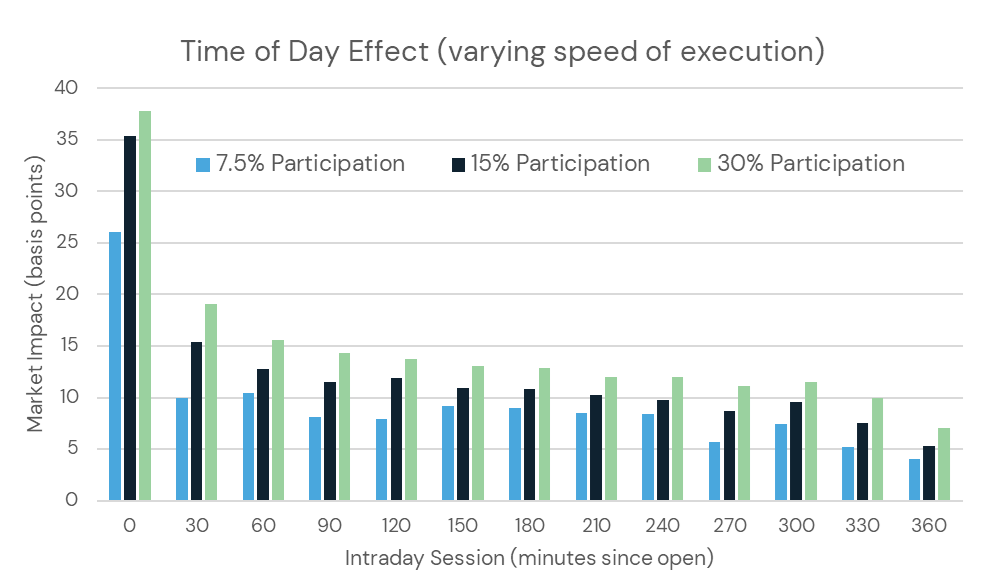

While IS Zero is an effective strategy for benefiting from the Time of Day Effect, more aggressive strategies may yield greater savings. Figure 2 suggests that trading in the last hour reduces costs despite higher participation rates, but execution data biases limit conclusions. To address this, we revisit TAQ data, comparing orders at 7.5%, 15%, and 30% participation rates while maintaining order size–constructing the sample just as before with these changes in participation.

Figure 5 confirms that backloading trades reduces costs, but indicates that participation rates are also critical. Trading at 30% participation in the last 30 minutes of the day costs half as much as trading between 10:00–11:00 and only 20% of the cost of the first 30 minutes. Avoiding high-cost bins and shifting volume to the last hour may lower costs despite higher participation rates. However, trading at twice the speed in the last 30 minutes isn’t always better than the last hour, as participation rate effects can outweigh time of day benefits. Balancing these factors is essential to optimizing cost.

Since making these discoveries, we have been collaborating with clients to tailor this effect to their trading styles. For example, experimenting with trading in low-cost time bins by using more bins for larger orders and fewer for smaller ones. During inactive periods in this experimental strategy, we trade opportunistically in block trading ATSs, delaying starts as blocks are executed. Early results from this dynamic strategy point to outperformance of IS Zero. As another example, we have customized liquidity-seeking strategies for several clients, reserving a significant portion of orders for the last hour of the day, which has resulted in substantial slippage reduction.

IS Zero+

As a result of this research, we’re building a new flavor of IS Zero called IS Zero+, which will optionally eliminate trading in high-cost bins based on order size and evaluate the trade-off between trading more in low-cost bins and increasing overall participation rates. Striking the optimal balance requires a robust market impact model capturing the interaction of time of day and participation rate. Driven by TAQ data as in the analysis above, we have achieved promising results in our execution cost model, Pulse, but further refinement is needed to ensure the model supports real-time trading decisions and not just transaction cost analysis.

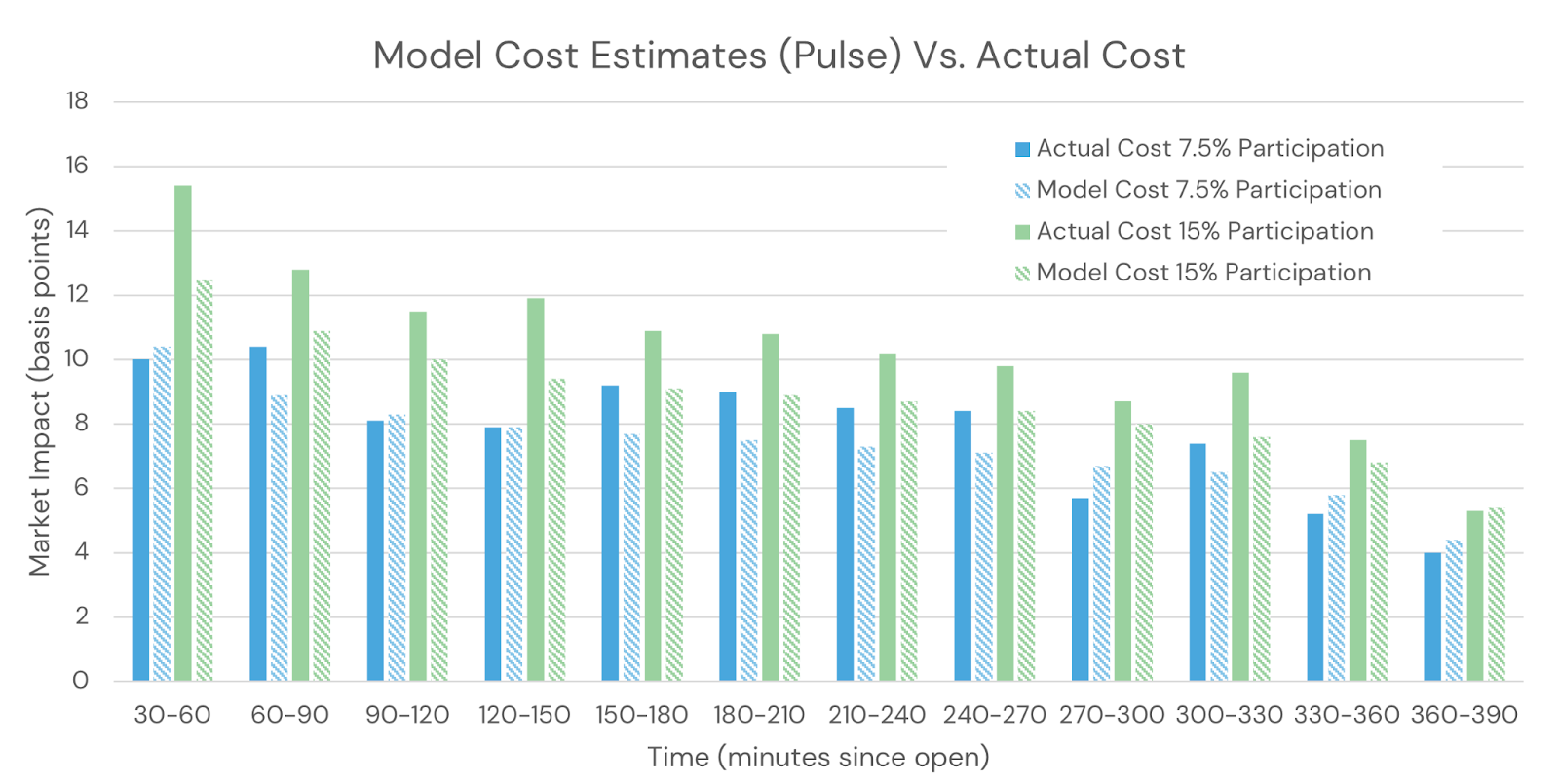

Figure 6 below shows the actual transaction cost versus model estimates of the cost for trading 1% of daily volume Russell 2000 constituent stocks at a 7.5% participation rate versus a 15% participation rate at varying times of day. In Figure 6, the solid bars represent actual costs and the striped bars represent model-estimated costs in Q1 2024 for comparison. Given highly refined market impact cost estimates, IS Zero+ can further reduce market impact costs systematically.

Conclusion

The Time of Day Effect offers a transformative opportunity to reduce trading costs, surpassing traditional optimization techniques in its potential impact. Leveraging TAQ and execution data, we have confirmed that trading costs vary significantly by time of day, with the last two hours consistently offering the lowest costs. Our IS Zero algorithm demonstrates practical success, reducing slippage across diverse order sizes, while more aggressive strategies like backloading trades or opportunistic block trading show even greater potential.

The development of IS Zero+ promises to further refine this approach, systematically balancing participation rates and time of day for optimal outcomes. As markets evolve, continuing to observe and systematically exploit the Time of Day Effect will be critical for traders seeking a competitive edge, driving measurable cost savings and enhancing execution efficiency.

Appendix

Table 1. Order size, daily volatility, average spread, and participation rates of stocks included in various bins for studying the Time of Day Effect using TAQ data as described above.

At BestEx Research, we care how you fill. We know from experience that systematic, quantitative decision-making around algorithm design contributes to globally optimal execution and results in significantly reduced execution costs. Reach out to us with questions at research@bestexresearch.com or learn more about us at bestexresearch.com.

This research paper reflects the views and opinions of BestEx Research Group LLC. It does not constitute legal, tax, investment, financial, or other professional advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell securities, futures, or other financial instruments or to engage in financial strategies which may include algorithms. This material may not be a comprehensive or complete statement of the matters discussed herein. Nothing in this paper is a guarantee or assurance that any particular algorithmic solution fits you, or that you will benefit from it. You should consider whether our research is suitable for your particular circumstances and needs and, if appropriate, seek professional advice.

Let us show you what's possible

Execution engineered to preserve your returns