Optimizing trading cost by leveraging "The Time of Day Effect"

Institutional traders using algorithms have long focused on cost-saving opportunities such as optimizing execution speed, improving order placement, curating liquidity, capturing short-term alpha, and minimizing latency. While these approaches have delivered incremental improvements, our recent research suggests that the timing of execution itself may offer a far greater opportunity to reduce trading costs.

The study, titled The Time of Day Effect, examines the variability in trading costs across the trading day, holding participation rate and order size constant. This effect is distinct from volume-driven effects, as many algorithms already spread orders proportionally in accordance with intraday volume. The findings indicate that executing the same order in the final hour of the trading session is consistently less costly than executing it earlier in the day.

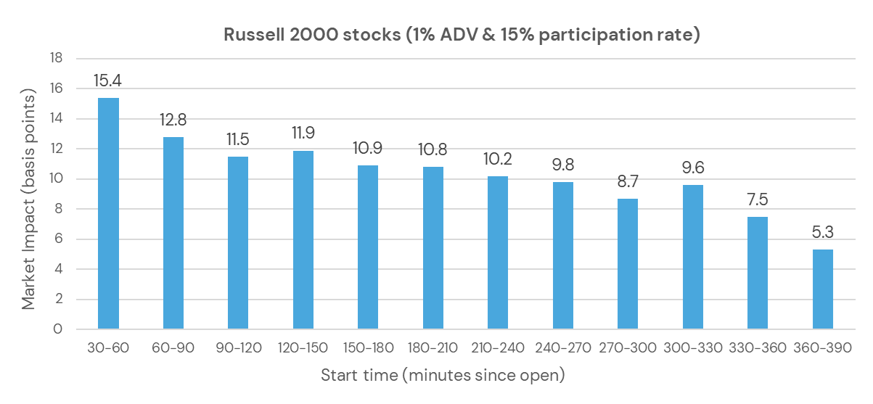

To quantify this effect we used Trade and Quote (TAQ) data to simulate trading 1% of daily volume in Russell 2000 constituent stocks at a fixed 15% participation rate. Figure 1 illustrates this effect, highlighting distinct cost profiles throughout the day. The analysis reveals that trading costs decline substantially as the session progresses, with the lowest market impact observed in the final two hours.

These results suggest that participation rate alone does not determine execution cost. Time of day exerts an independent and significant influence. While most execution algorithms use intraday volume as a proxy for liquidity, the data shows that volume does not fully explain where and when liquidity is cheapest.

To validate these results with live execution data, we analyzed approximately 635,000 parent orders from four years of trading, excluding canceled and passive limit orders. We compared full-day orders with those initiated in the final hour of the session and it corroborates the TAQ-based findings, in striking fashion.

The research paper further explores the robustness of the Time of Day Effect across stocks with varying liquidity profiles. It also outlines multiple approaches to exploit the effect to reduce algorithmic execution costs. One of these approaches has already been incorporated into our flagship algorithm IS Zero, which shifts more trading activity into low-cost time intervals. A second, more aggressive variant—IS Zero+—is currently in development. It aims to systematically avoid high-cost periods altogether, using a proprietary market impact model to balance participation rate and timing systematically.

To learn more about how our algorithms capitalize on the Time of Day Effect, request the full research paper using the form below.