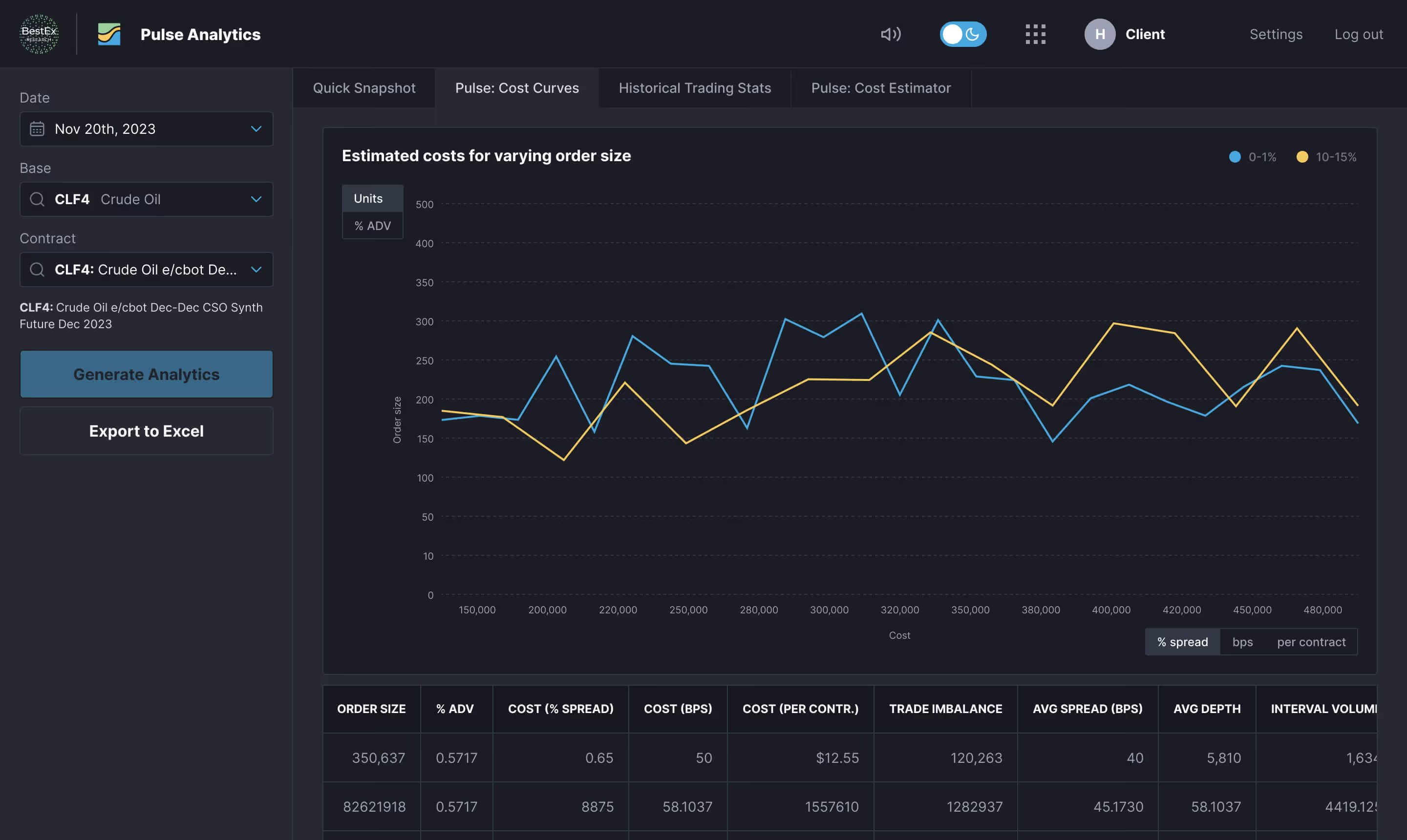

Cost-estimator-fixed-duration

Provides estimated cost of trading a specified contract from a specified start time to a specified end time for specified order size.

Notes:

1) If end time is specified beyond market close, the model will assume order ends at market close and increase participation to complete order accordingly. All output will align with this change.

2) "trailing days" & "val" parameters are optional, with default values indicated below. All other parameters are required.

start_time

Start time of the intraday period in the format HH:MM:SS

end_time

End time of the intraday period in the format HH:MM:SS

ordersize

Size of the order (no. of contracts)

exchange_symbol

Enter exchange symbol of contract

futures_base_symbol

Respective base symbol. Must align with the exchange symbol

date

Date to estimate for in the format YYYY-MM-DD. For historical, no more than one year prior

trailing_days

Number of previous days to include in estimated analytical inputs to model (default value n=7). Larger values require more estimation time; we recommend limiting to 30 days

val

Use 'n' for estimated model inputs (e.g., estimated spread, depth, etc.). For realized data as model inputs use 'y'; this option is available for historical dates only. Default value: 'n'

Cost-estimator-fixed-participation

Provides estimated cost of trading a specified contract at a specified start time with specified participation rate and order size.

Notes:

1) If the estimated end time is beyond market close, model will assume order ends at market close and increase participation to complete order accordingly. All output will align with this change.

2) "trailing days" & "val" parameters are optional, with default values indicated below. All other parameters are required.

start_time

Start time of the intraday period in the format HH:MM:SS

participation

Enter participation rate (0.0 - 1.0)

ordersize

Size of the order (no. of contracts)

exchange_symbol

Enter exchange symbol of contract

futures_base_symbol

Respective base symbol. Must align with exchange symbol

date

Date to estimate for in the format YYYY-MM-DD. For historical, no more than one year prior

trailing_days

Number of previous days to include in estimated analytical inputs to model (default value n=7). Larger values require more estimation time; we recommend limiting to 30 days

val

Use 'n' for estimated model inputs. For realized data as model inputs use 'y'; this option is available for historical dates only. Default value: 'n'

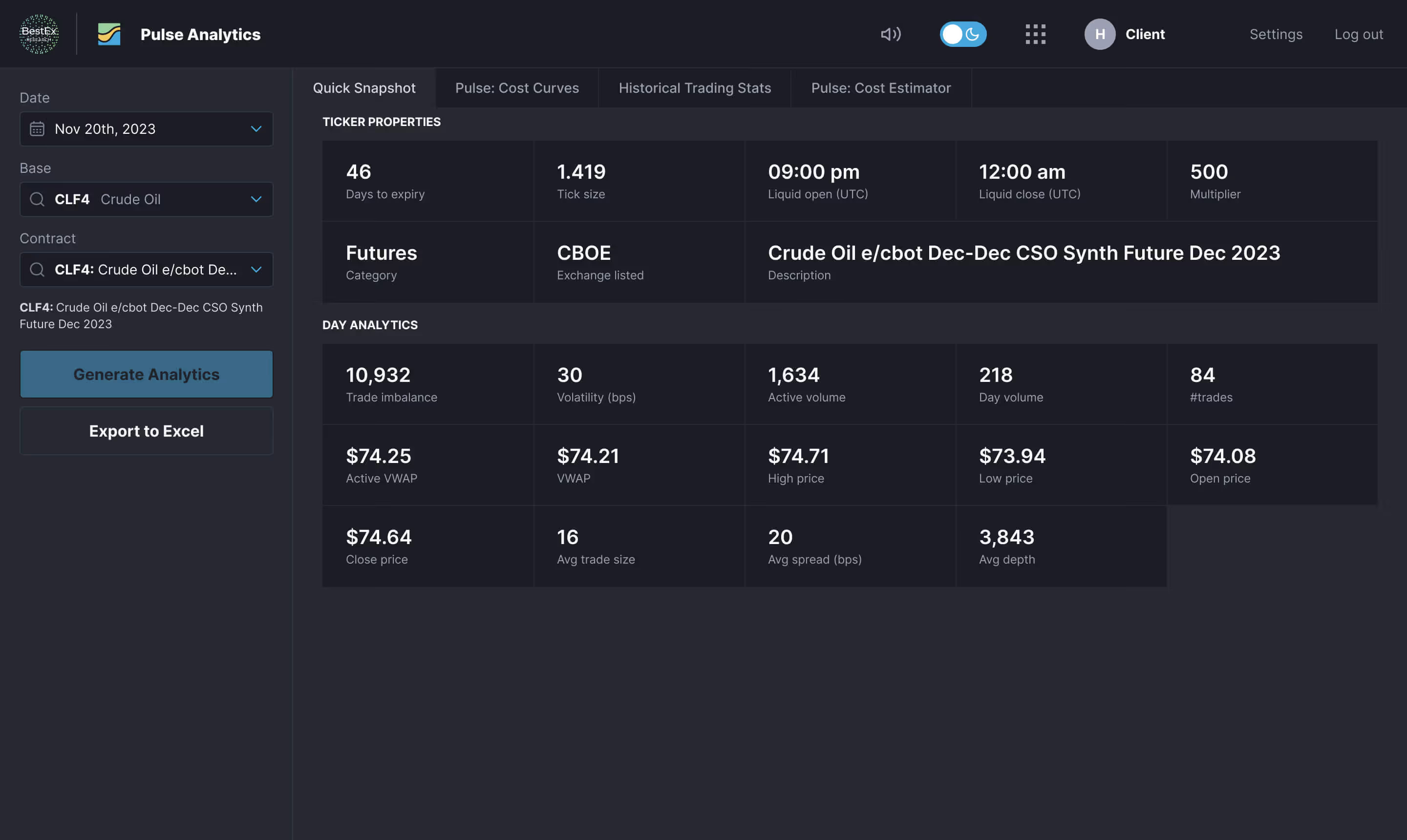

Estimated stats

Provides estimated analytics for a specified product from a specified start time to a specified end time.

Notes:

"trailing days" & "val" parameters are optional with default values indicated below. All other parameters are required.

start_time

Start time of the intraday period in the format HH:MM:SS

end_time

End time of the intraday period in the format HH:MM:SS

exchange_symbol

Enter exchange symbol of contract

date

Date in format YYYY-MM-DD. For historical, no more than one year prior

trailing_days

Number of previous days to include in estimated analytics (default value n=7). Larger values require more estimation time; we recommend limiting to 30 days

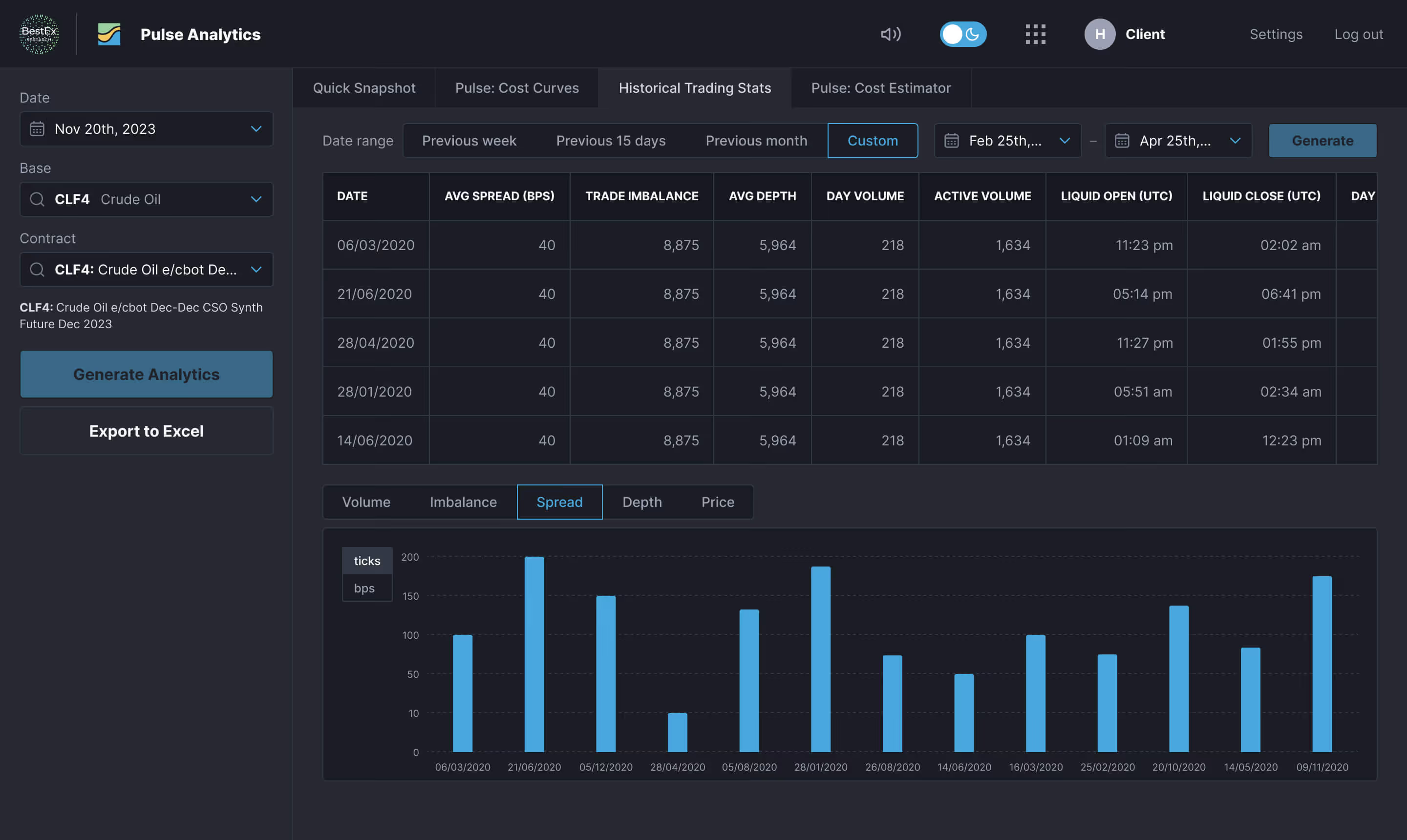

Realized stats

Calculates the realized analytics (historical) for a specified exchange symbol from aspecified start time to a specified end time.

All parameters are required.

start_time

Start time of the intraday period in the format HH:MM:SS

end_time

End time of the intraday period in the format HH:MM:SS

exhange_symbol

Enter exchange symbol

date

Date in format YYYY-MM-DD; no more than one year prior

Daily trading stats

Provides realized daily analytics for a specified exchange symbol from a specified start date to a specified end date.

All parameters are required.

exchange_symbol

Enter exchange symbol to fetch respective trading stats

start_date

Start date of range in the format YYYY-MM-DD; no more than one year prior

end_date

End date of range in the format YYYY-MM-DD; no more than one year prior

Active-instruments

Provides a list of contracts (varying expiries) traded on a given day for a specified base symbol; if no active instruments are found, “None” is returned.

All parameters are required.

futures_base_symbol

Base symbol for which to fetch active contracts

date

Active date of contracts to be returned in the format YYYY-MM-DD. For historical, no more than one year prior

Supported-symbols

Provides a list of base symbols supported by the API.

This function takes no parameters