We care how you fill.

Reducing transaction costs with unconflicted,

research-driven execution algorithms

for global markets

Futures market structure is nuanced and unique.

Achieving best execution requires rigor.

Research-driven product innovation

Our innovations around shadow liquidity, calendar spreads, rolls, and more all started as research questions. Before we build, we find the root cause of a problem, study market data and simulate solutions.

Fill-level scrutiny

As we optimize algo performance, we examine individual fills across contracts, times of day, volatility regimes, and urgencies. This painstaking analysis helps us derive the right strategies for your flow.

Evolution with markets

For us, algorithm design is a process that meets the moment, not a one-time project. As markets change, strategies must be adapted to continue delivering optimal outcomes.

An extension of your trading desk

The same people who drive our research work as an extension of your trading desk to optimize for your unique order flow. We're laser-focused on your trading from the moment orders arrive through post-trade TCA.

Problem-centered research unique to futures powers every algorithm we offer

Roll cycle and curve-aware analytics

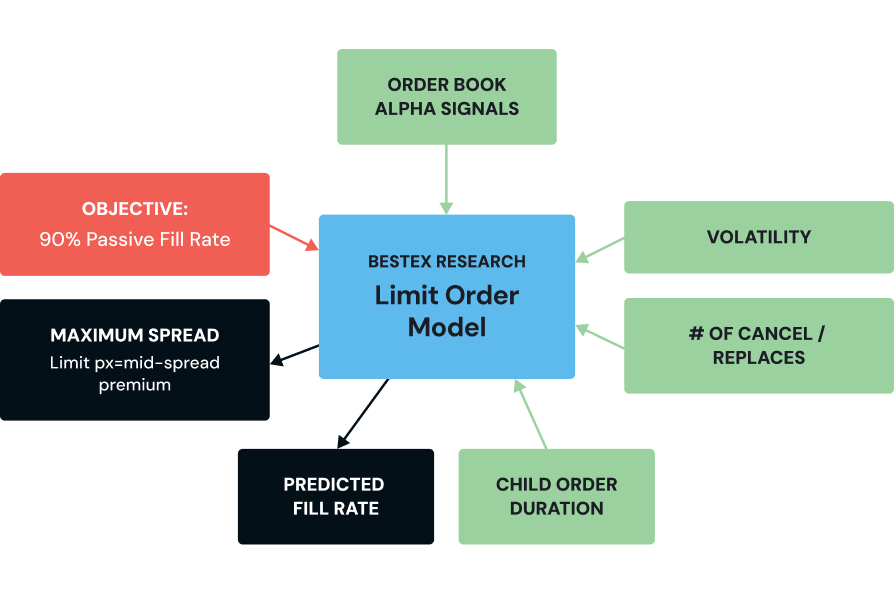

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Adapts across asset classes

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Opportunistic liquidity-taking

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Shadow liquidity for back-month contracts

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Optimized for calendar spreads & rolls

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Smart order book laddering

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Optimized for each exchange's matching rules

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Proprietary limit order model

Standard industry algorithms rely on simple heuristics for limit order placement, frequently repricing orders without accounting for order book alpha, volatility, trade frequency or time needed to fill a child order. This results in suboptimal spread capture and increased adverse selection.

BestEx Research integrates a proprietary Limit Order Model into all of its algorithms, leveraging academic research and market expertise to price limit orders more effectively. Inspired by options theory, our approach optimally prices passive orders, adjusting for expected adverse selection and maximizing spread capture.

Spread Capture by product category for orders with participation rate <5%

Strategies engineered to minimize transaction costs

IS Zero

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 30%.

Adaptive Optimal

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 30%.

TASClose

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 30%.

POV

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 30%.

VWAP

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 30%.

TWAP

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 30%.

Close

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 30%.

Built for the nuances of global market structure

Seamlessly integrated with major EMS/OMS and FCMs, trading 150+ contracts across 21 global exchanges

North America

- CBOE

- CBOT

- COMEX

- CME Group

- ICE US

- MIAX

- NYMEX

- TMX Futures

Europe

- ICE Europe

- ICE Endex

- Eurex

- Euronext Paris

Euronext Amsterdam

Asia Pacific

- ASX

- HKEx

- SGX

- Osaka Exchange

Latin America

- B3

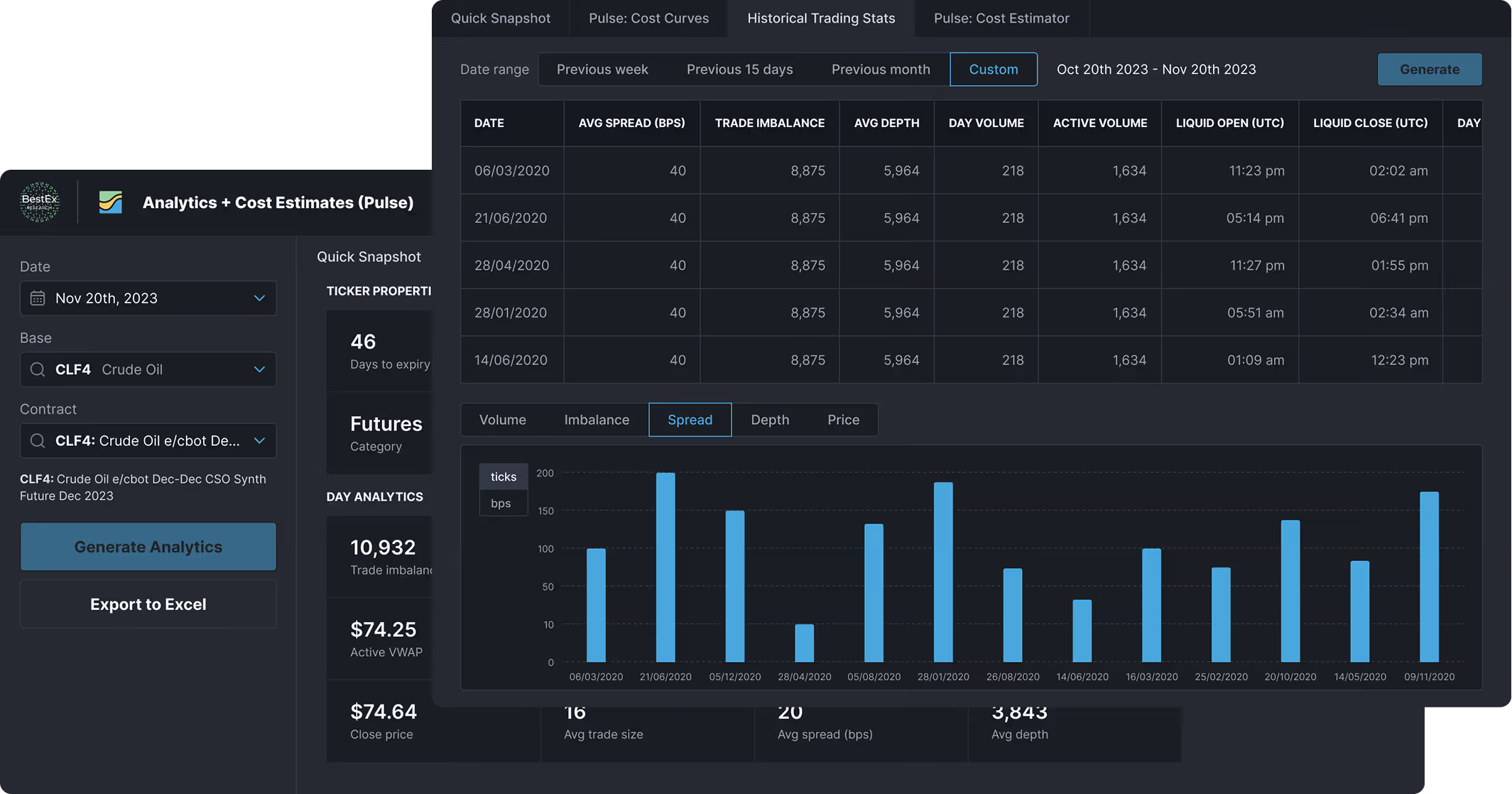

Pulse: Market impact model & pre-trade analytics

Available via REST API & AMS One

An end-to-end platform that supports your execution

Trading Dashboard

Real-time visibility into every order, fill, and venue interaction as it happens. Progress, performance, and alerts in a single view.

Strategy Studio

Speedy customizations to your algo strategies to match your specific flow, urgency, and benchmark. Changes go live overnight.

TCA

Fully integrated TCA supports analysis at the parent order and fill level, broken down into appropriate views for actionable insights.

Pre-Trade

Estimated trading costs and analytics before you trade. Our proprietary market impact model is built from ground up for each asset class for more accurate results.

.svg)

Simulator

A realistic exchange simulator tests strategy changes before they go live. Test against months of tick data in hours for success on day one.

let us show you what's possible

Execution engineered to preserve your returns