We care how you fill.

Reducing transaction costs with unconflicted,

research-driven execution algorithms

for global markets

In an increasingly complex market structure, achieving best execution requires rigor

Research-driven product innovation

Our limit order model, dark framework, and queue-jumping logic all started as research questions. Before we build, we find the root cause of a problem, study market behavior and simulate proposed solutions.

Fill-level scrutiny

As we optimize algo performance, we examine individual fills across venues, times of day, volatility regimes, and urgencies. This painstaking analysis helps us derive the right strategies for your flow.

Evolution with markets

For us, algorithm design is a process that meets the moment, not a one-time project. As markets change, strategies must be adapted to continue delivering optimal outcomes.

An extension of your trading desk

The same people who drive our research work as an extension of your trading desk to optimize for your unique order flow. We're laser-focused on your trading from the moment orders arrive through post-trade TCA.

Transparency in every layer of execution

Execution algorithms don't have to be a black box. Our research for buy-side clients shares the evidence behind our algorithm design, mapping the journey from the root of the problem to the solution we provide.

Problem-centered research powers every algorithm we offer

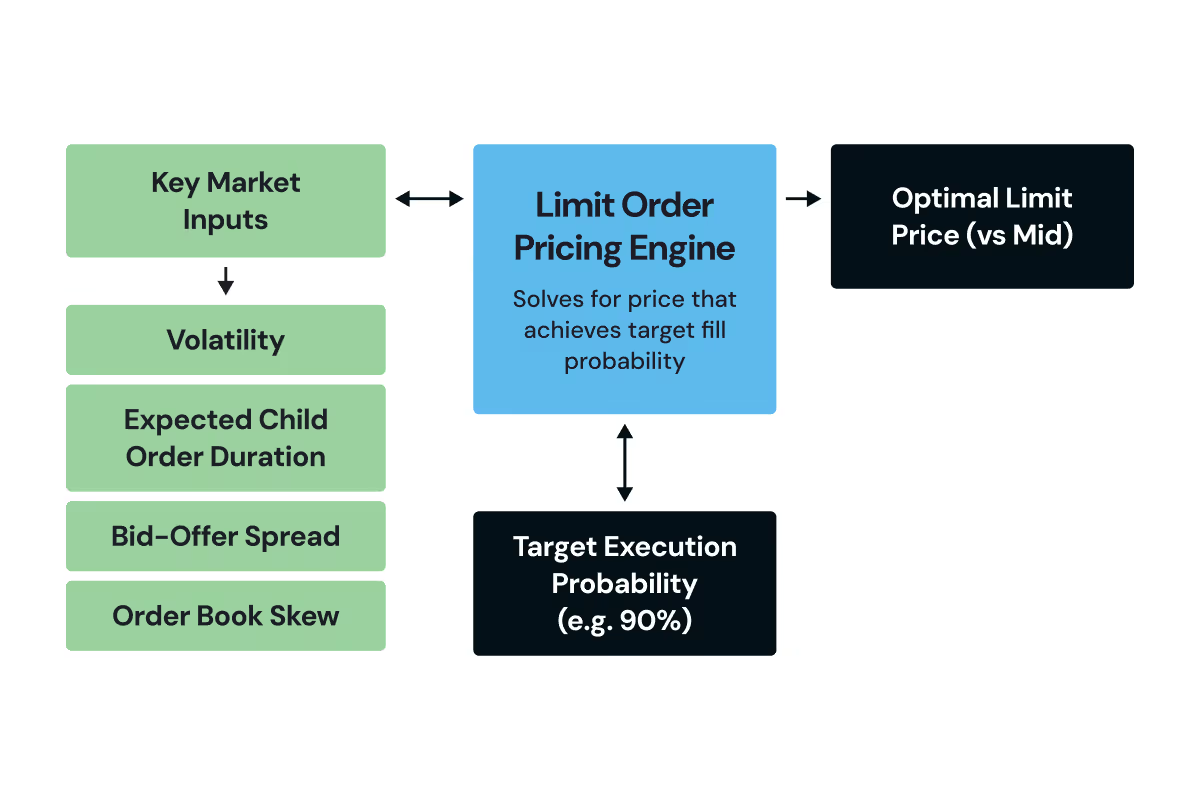

Most algos use heuristics that reprice limit orders without accounting for liquidity or volatility, inflating the cost of every passive fill.

The heart of our algorithms is a proprietary limit order model, grounded in academic research, pricing limit orders similarly to options theory, optimally accounting for expected adverse selection and maximizing spread capture.

The BestEx Research limit order model takes in the characteristics of the product being traded, including volatility, speed of trading, and more, and returns a recommended limit price for each child order with the specified fill probability.

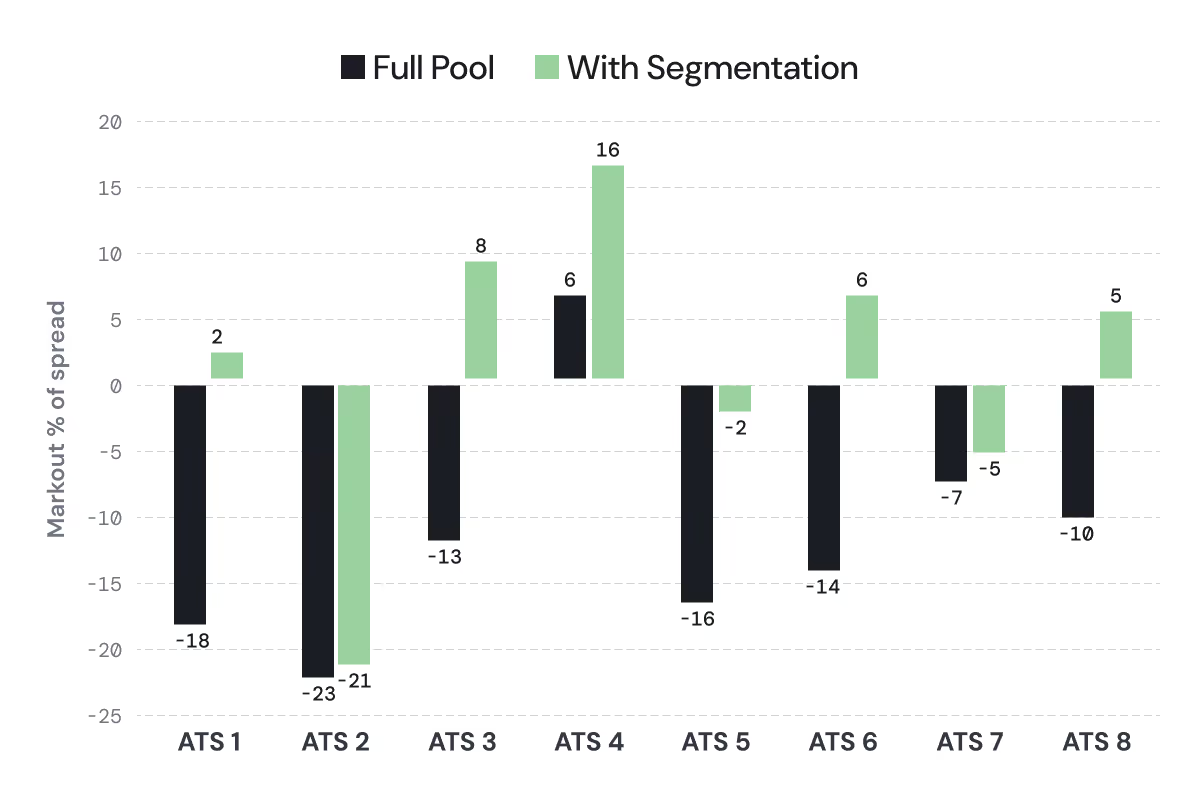

The ATS landscape has evolved, increasing toxicity and information leakage and leading to higher trading costs.

Our dark liquidity curation framework incorporates ATS segmentation, tactic selection, proprietary signals, and conditional orders strategically to avoid toxic interactions and minimize information leakage. Curator, our dark algorithm, is built on this framework.

Venue segmentation is effective but the magnitude varies. The chart above illustrates comparison of Full Pool to Tier 1 (highest quality) at corresponding pool.

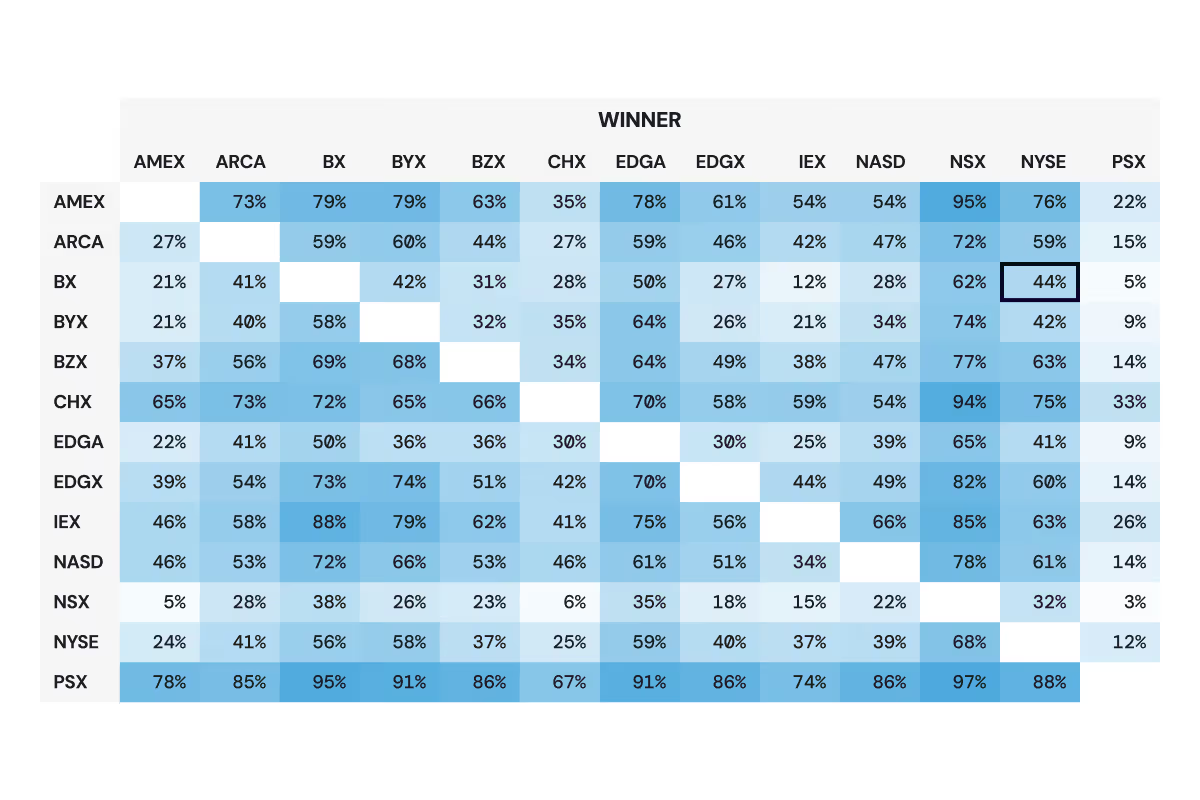

In a fragmented market with many exchanges, even an optimally priced child order can languish in a long or slow-moving exchange queue and face high adverse selection.

Our proprietary queue-jumping logic evaluates over 65,000 combinations of top-of-book exchanges, ranking venues by their likelihood of attracting market orders so our algo orders can jump the queue and avoid adverse selection. This model supports all algorithms trading on exchanges.

The WinMatrix summarizes exchange competitiveness. The black box highlighted above indicates that for this stock, NYSE receives a market order 44% of the time when it and NASDAQ BX are competing (BX is inverted).

Execution Consulting

We believe in partnership and a consultative approach because what's best for each client isn't always available off the shelf.

Our team of seasoned algorithmic trading and market structure practitioners work alongside your desk to sharpen every aspect of your execution. Paired with nimble strategy customization and deeply integrated TCA, we deliver actionable insights that don't just measure performance. They improve it.

Strategies engineered to minimize transaction costs

IS Zero

Curator

Adaptive Optimal

POV

VWAP

TWAP

Close

Built for the nuances of global market structure

United States

Canada

Europe

APAC

Built and tested for United States equity market structure

- Execution logic based on US equities market structure expertise paired with empirical research

- Extensive off-exchange venue coverage, accessing more than 97% of dark liquidity

- Robust estimation of critical values impacting trading decisions such as spread, depth, volume, and volatility including a hybrid machine learning methodology that adopts a mix of stock-specific and group-based volume profiles

- Proprietary limit order placement model honors the volume and volatility signature of each stock for maximal spread capture given child order urgency

- Queue-jumping methodology optimizes limit order placement across US equities exchanges

- Curator, a research-driven framework for dark execution, navigates the layered complexity of ATSs including segmentation, tactic selection, signals, minimum quantities, and more to reduce information leakage and adverse selection

Built and tested for Canadian equity market structure

- Our platform is differentiated by its intelligent handling of interlisted stock, accessing liquidity in both US and Canadian markets and returning all fills in Canadian dollars

- For the 260 current interlisted names, a median of 58% of daily liquidity is found in US markets, with 10% of stocks having more than 80% of their liquidity in US markets

- For POV and VWAP algorithms, participation rate and volume cap parameters can be specified for:

- Canadian volume only

- US volume only

- Both US and Canadian volume

- For these stocks, we access all available Canadian liquidity and all dark pools and exchanges in the US

Built and tested for European equity market structure

- Robust order placement tested against months of tick data and European exchange Simulator

- Incorporates market data feeds from all MTFs and exchanges in each country for optimal use of Primary vs. EBBO, locked and crossed quotes handling

- Unique auction logic built to handle each exchange/MTF rules and market structure

- Access to most MTFs, SIs, Periodic Auctions, and Conditionals via advanced liquidity-seeking logic

- Advanced liquidity providing and taking logic is built into our fully customizable SOR

- Handling rules such as Large-In-Scale (LIS) waivers, reference price waivers (RPW), and liquidity-based waivers

- Realtime and historical analytics account for each market’s idiosyncrasies, for example: on-exchange vs. off-exchange volume and proper tick size handling

Built and tested for APAC equity market structure

- Execution logic tailored to each specific market structure paired with research and empirical observation

- Market-specific analytical profiles for robust estimation of critical values impacting trading decisions such as spread, depth, volume, and volatility

- Proprietary limit order placement model honors the volume and volatility signature of each stock for maximal spread capture given child order urgency

- Limit order placement incorporates stock-specific queue lengths, layering orders in the limit order book to optimize passive fills; flexibility around schedule is increased as needed to accommodate passive fills on long-queue stocks

An end-to-end platform that supports your execution

Trading Dashboard

Real-time visibility into every order, fill, and venue interaction as it happens. Progress, performance, and alerts in a single view.

Strategy Studio

Speedy customizations to your algo strategies to match your specific flow, urgency, and benchmark. Changes go live overnight.

TCA

Fully integrated TCA supports analysis at the parent order and fill level, broken down into appropriate views for actionable insights.

Pre-Trade

Estimated trading costs and analytics before you trade. Our proprietary market impact model is built from ground up for each asset class for more accurate results.

.svg)

Simulator

A realistic exchange simulator tests strategy changes before they go live. Test against months of tick data in hours for success on day one.

let us show you what's possible

Execution engineered to preserve your returns